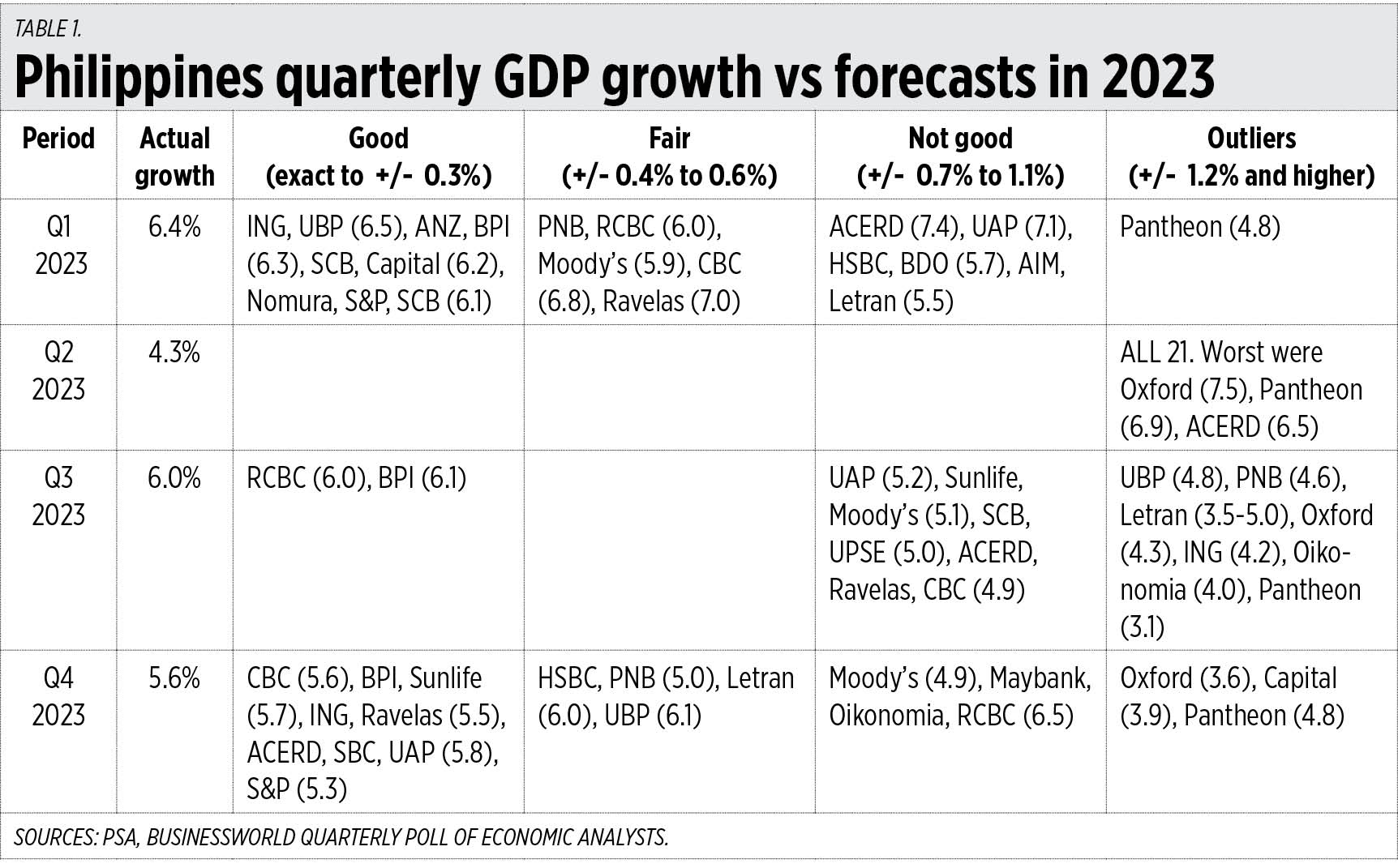

Growth forecasts vs actual growth, and agriculture performance

Among the important reports published in BusinessWorld is the quarterly poll of economists and analysts on their GDP growth forecast, reported few days before the Philippine Statistics Authority (PSA) releases the official GDP data. This is on top of the monthly poll of the same group of economists and analysts for the monthly inflation rate forecasts.

I checked the infographics and reports on the quarterly GDP growth forecast polls for all four quarters of 2023 and came up with an analysis.

The forecasters are the chief economists of banks and consulting firms or one of the faculty members of academe. They are from banks, consulting and finance firms, and the academe.

The organizations were: Bank of the Philippine Islands (BPI), Banco de Oro (BDO), China Banking Corp. (CBC), ING Bank NV, Maybank Investment Banking Group, Philippine National Bank (PNB), Rizal Commercial Banking Corp. (RCBC), Security Bank Corp. (SBC), Standard Chartered Bank (SCB), Union Bank of the Philippines (UBP) for the banks; ANZ Research, Capital Economics, HSBC Global Research, Moody’s Analytics, Nomura, Oikonomia Advisory & Research, Inc., Oxford Economics, Pantheon Macroeconomics, Ravelas (eManagement for Business, later Reyes Tacandong & Co.), S&P Global, Sunlife Investment Management & Trust Corp., for the consulting and finance firms; and, the Asian Institute of Management (AIM), Ateneo Center for Economic Research and Development (ACERD), Colegio de San Juan de Letran Graduate School, De La Salle University (DLSU), University of Asia and the Pacific (UA&P), and the University of the Philippines School of Economics (UPSE) for the academe.

I created a category based on how near or how far the forecasts were from the actual growth, represented by “plus or minus” (+/-). “Good” forecasts are those with an exact number and those +/- 0.3%. “Fair” forecasts are those with +/- 0.4% to 0.6% from the actual GDP. “Not Good” are those with +/- 0.7% to 1.1%, and “Outliers,” or far out forecasts, are those +/- 1.2% or higher.

Not all economists and analysts participated in the quarterly poll, some participated in Q1, but not in Q2 or Q3, but on average, 21 to 23 analysts join the quarterly poll.

Q2 of 2023 is notable because all the analysts were wrong and gave outlier forecasts. Q1 and Q4 had many analysts forecasting correctly (see Table 1).

{kind=link}

So the best forecaster is BPI’s Emilio “Jun” Neri, with three out of four forecasts that were good. Congrats Jun and the team, you are brilliant. The organizations with the greatest number of outlier projections are Pantheon (4 of 4, with no good forecast) and Oxford (3 of 4).

This exercise shows that in general, human action and reaction to certain natural and social changes are still far from being accurately predicted by humans and trained professionals, no matter how elaborate and modern the mathematical models and tools they use are. That is why government and multilaterals’ central planning, one-size-fits-all policies are likely to produce more harm and disaster than the stated goals.

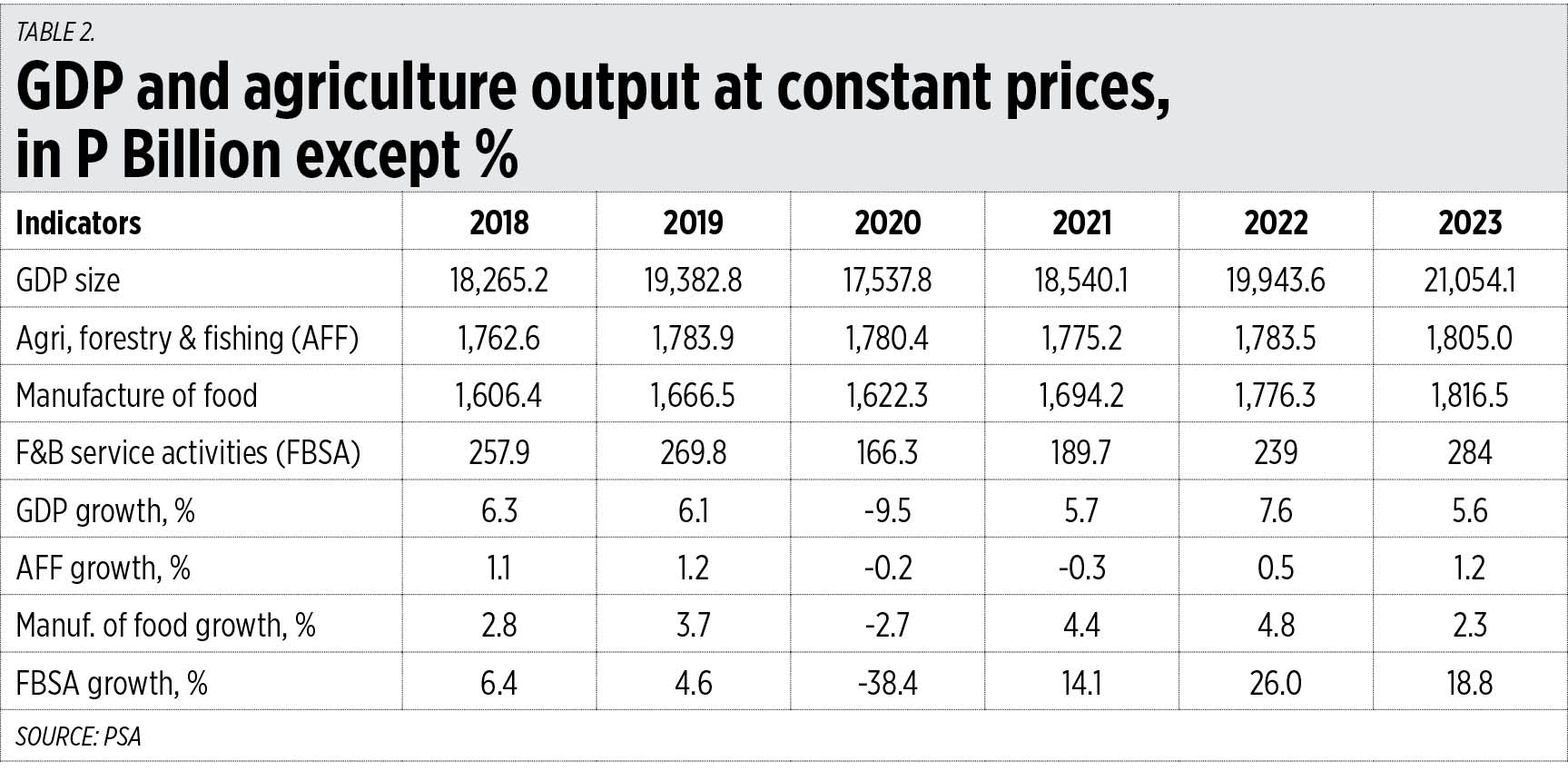

3 MEASUREMENTS OF AGRICULTURE PERFORMANCE

There are at least three ways to measure the performance of the agriculture sector. The first is the Agriculture, Forestry and Fishing (AFF) sector in the GDP by industrial origin or GDP by supply side. The second is manufacturing of the food products sub-sector under the industry sector. And the third is the food and beverage service activities (FBSA) sub-sector under the services sector.

We must look at the two sub-sectors because there is heavy underreporting in the output of raw agricultural, animal, and fishery products as shown by AFF growth which is always very low, with a maximum 1.2% growth in the last six years even if overall GDP grew by 7.6%.

Growth in the manufacturing of food products reached 4.8% in 2022. This is not possible if there was no growth of at least a similar level in raw agricultural products. So, by proxy, AFF should be growing 2.3% to 4.8%, not just 0.5% to 1.2% as officially recorded.

FBSA is a better proxy because it includes directly cooked and served food like those in restaurants, hotels, carinderia and litson-manok stalls. Meaning non-manufactured, preserved, and canned foods are included. Annual growth in FBSA was 4.6% to 26% (see Table 2).

{kind=link}

So, if AFF output is actually growing by 4% to possibly 26% and not 0.5% to 1.2%, then many agricultural subsidies and freebies (free irrigation, free tractors, free seeds, etc. with no timetable to end the subsidy) and the large and elaborate agricultural bureaucracies may not be justified. Instead, the government should focus on more rural infrastructure like longer and wider paved barangay roads that benefit everyone, not just farmers and fisherfolks.

Related here are taxation and energy policies that distort agricultural production. Like the imposition of diesel tax — from zero to P6/liter under the TRAIN law of 2017 (RA 10963) implying that expensive diesel for tractors, harvesters, trucks, irrigation pumps, fishing boats is necessary to “save the planet.”

Then there is a growing trend of land conversion from agriculture to solar farms. This has short- to long-term adverse impact on food production and food inflation. This must stop. Expanding food production, saving the poor and hungry, should be prioritized over “saving the planet” because the weather is uncertain.

Bienvenido S. Oplas Jr. is the president of Bienvenido S. Oplas, Jr. Research Consultancy Services, and Minimal Government Thinkers. He is an international fellow of the Tholos Foundation.