How MSMEs can be protected from predatory lenders

{kind=link}

{kind=link}

{kind=link}

By Bernadette Therese M. Gadon, Researcher

JESSICA DELA, 60, got a bank loan to start her liquefied petroleum gas (LPG) franchise.

However, she said that she wouldn’t accept the loan if her first business — a refreshment kiosk — isn’t stable.

For her, she advised new business owners, especially small business owners, to prepare beforehand, and only resort to lending when you need an additional revolving funds or you can ensure your business or other income can cover for your loan, because there are no guarantees on a startup to bring profit right away.

Latest data from the Department of Trade and Industry’s (DTI) 2022 Philippine MSME Statistics showed 99.59% of total businesses in the country are MSMEs, with 90.49% falling under microenterprises.

In an e-mail interview with the Department of Trade and Industry Regional Operations Group (DTI-ROG) it defined micro, small, and medium enterprises (MSMEs), per the Magna Carta for MSMEs, as any business activity or enterprise, whether single proprietorship, cooperative, partnership or corporation, whose total assets are not more than P3 million (micro business), P3 million-P15 million (small), and P15 million-P100 million (medium).

Additionally, its Barangay Micro Business Enterprise (BMBEs Act of 2002), who caters to microenterprises, also adapted its definition to any businesses whose total assets are not more than P3 million.

With a huge chunk of these businesses falling under services, such as retail stores and sari-sari stores, most Filipino business owners survive on profits accumulated from their business to either restock or expand said business.

The country’s economic landscape was heavily affected this year from base effects of inflation from the COVID-19 pandemic, and geopolitical tensions that started last year bringing prices of goods and services up, which cascaded to smaller businesses in the Philippines.

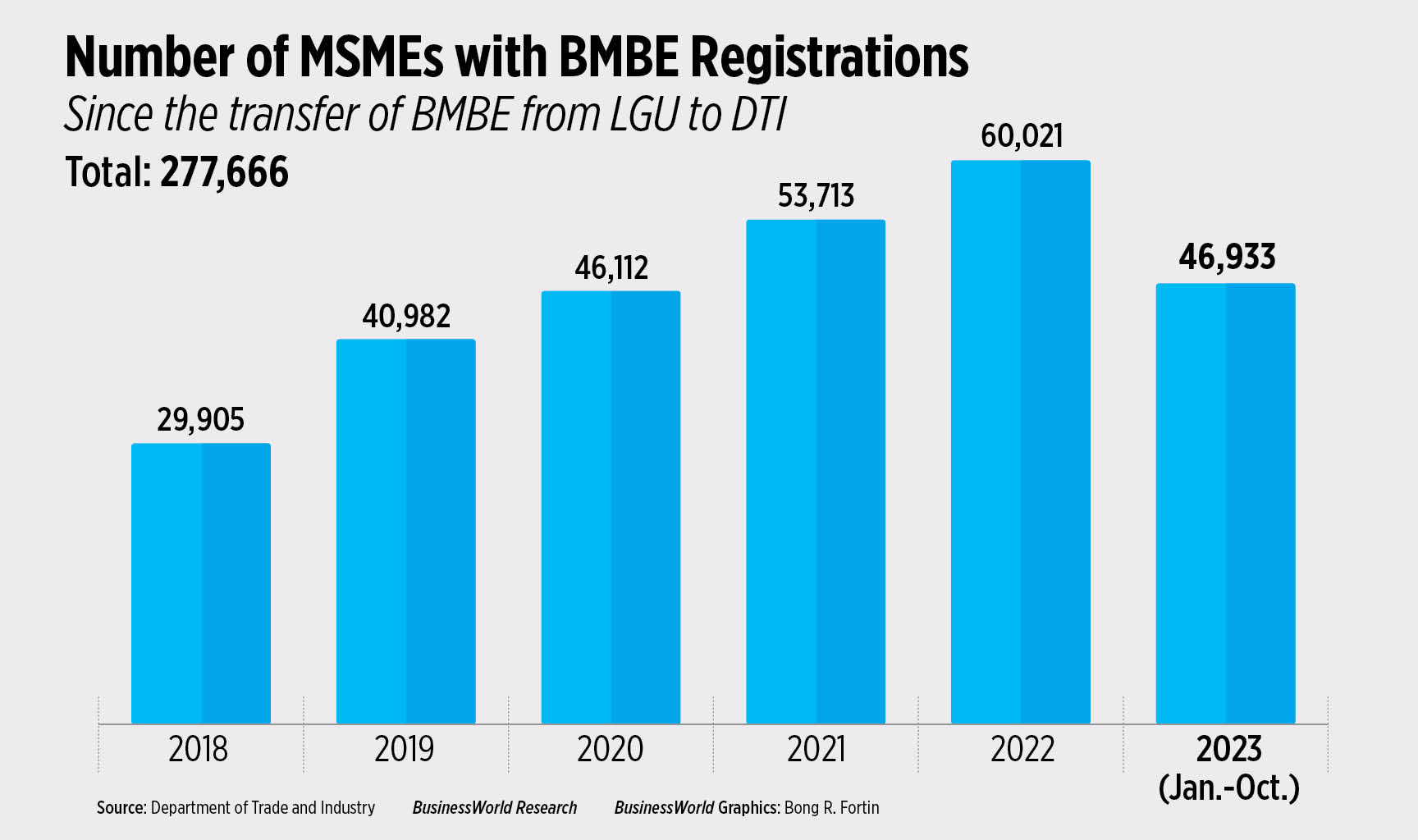

Data from the DTI-ROG showed a total of 277,666 BMBE registrations since the transfer from local government units (LGU) to Negosyo Centers.

A total of 46,933 BMBEs have been registered from January to October, down from 60,021 registrations as of end-2022.

“A 2021 survey commissioned by the Asian Development Bank (ADB) among 1,000 respondents revealed that access to credit and capital, after access to markets, continues to be the second most significant barrier to growth for MSMEs,” the Bangko Sentral ng Pilipinas (BSP) said in an e-mail exchange.

With MSMEs not needing to loan, the central bank said that these small businesses rely mostly on self-funding or funding through family and friends.

With limited resources of owners to improve their business, some have opted to lending to start or grow their business. However, how safe is it for MSMEs to lend in the Philippines?

MSME LENDING LANDSCAPE

Ms. Dela said that she was not aware of how rampant illegal lending companies are in the country. While she received offers online on lending offers, she did not see the need to avail of those offers because she already received a loan offer from her bank and is aware of different loan programs from other well-known banks.

As a government agency handling and ensuring fair competition of businesses in the country, the DTI-ROG addressed usurious or predatory lending practices by “(1) providing legitimate financial services that further disincentive small businesses to avail of illegal lending companies, and (2) enhancing information dissemination for better informed borrowers.”

“In terms of information dissemination against illegal lending, the Credit Information Corp. (CIC) publicizes the efforts of the Bangko Sentral ng Pilipinas (BSP) and Securities and Exchange Commission (SEC). In particular, [the] SEC is conducting a crackdown on unauthorized and abusive online lending activities,” the DTI-ROG said.

In an e-mail exchange, Union Bank of the Philippines (UnionBank) Business Banking Head Senior Vice-President Jaypee Soliman said that UnionBank offers different products for different MSMEs such as their Supply Chain Financing program wherein they provide a revolving credit facility to MSMEs within the system.

“We use data driven and alternative data models plus relationship data to assign credit limits and provide funding even on a per transaction basis. This allows full control and flexibility to the MSME, as they are not tied fully to a term, but they have the ability to draw and pay as needed and as funds are collected,” Mr. Soliman said.

“This is what truly sets us apart. Our ability to collect data that gives us a better understanding of the MSME and be used in credit models that no longer requires massive documentary and long assessment periods,” he added.

Once a business has been registered under BMBE, they can seek services of capacity building, technology transfer, financing support, and market access assistance through Negosyo Centers around the Philippines, the DTI-ROG said.

Furthermore, certified BMBEs are eligible for income tax exemptions from the Bureau of Internal Revenue and exemption from the coverage of minimum wage by the Department of Labor and Employment.

While many programs are available for all kinds of MSMEs in the country, Ms. Dela said that she started her first business using her own money because she did not meet the criteria of most banks.

“I was offered a loan for my second business because I already had a record in the bank from my first business, [and] saw how capable it is, and they saw that I deposit every day,” she said.

According to the DTI-ROG, prior to the Go Negosyo Act, BMBE registration was coursed through LGUs which required nine documentary requirements. With the BMBE transferred through Negosyo Centers, businesses only need to present two requirements (business certificate and registration form) to be certified.

For UnionBank, Mr. Soliman said that they accommodate small businesses by credit scoring them through alternative models, and using those data to allow businesses who does not have access to collateral to be able to borrow.

“We are able to expand the ability of a small and even a micro business to access formal lending, which is hard to do for them.”

“As a bank, we also educate small business owners or negosyantes on how they can fully manage their financial data through digitization of their accounting, collections, and so on, which later on builds a ‘digital footprint’ for them that is used in alternative credit,” Mr. Soliman said.

Moreover, for small businesses who do not meet most banks’ criteria, Mr. Soliman said that there are platforms such as SeekCap, a hub of financial institutions in the Philippines where borrowers can register to gain access for easier search on various institutions where businesses can meet its criteria.

Despite the innovation of technology to make lending easier for small businesses, predatory lenders also adapted online to scam business owners.

For businesses that have been scammed already, Mr. Soliman said that rebuilding your business can help you in applying to legal lenders. With alternative data, UnionBank will use data points of the business, its operations, collections, and financial behavior to assess whether a business can be granted a loan.

“Businesses who might not be able to meet some of the alternative criteria would have an option to provide additional security to their loan such as real estate,” Mr. Soliman added.

The DTI-ROG recommended MSMEs to apply for loans via Small Business Corp. (SB Corp.) through its RISE UP Micro Multi-purpose Loan where microenterprises can borrow up to P300,000 payable monthly up to three years.

Loans through the SB Corp. only have four requirements, namely: a government-issued ID, photos and videos of business operations and assets, corporate documents (if applicable), and barangay certificate (for P100,000 and below loans)/BMBE certificate or Mayor’s permit (for above P100,000 loans).

With inflation rising this year affecting goods and services, businesses also bear the brunt of the effects to adjust their prices that can accommodate both their business’ needs, as well as keeping it low to avoid passing the expense to their customers.

Ms. Dela said that because her business is a franchise, she has no say on price movements of LPG products. Her option is to text blast her customers on price changes prior the implementation to let them know ahead if the LPG price increases or decreases, helping her customers decide when to order.

TIPS FOR A WISER NEGOSYANTE

Mr. Soliman said to watch out for “too-good-to-be-true” programs, and as a negosyante, doing research on various lending offers or finding a fellow experienced negosyante or business communities to provide feedback and guidance, can help to make sure businesses won’t be tricked.

He also noted that UnionBank provides platforms for community building such as the UnionBank Globallinker.

“This platform allows you to connect with more than 80,000 MSMEs in the Philippines, and even access more than 500,000 MSMEs around the world. We also provide access to MSME support such as educational webinars and trainings, technology service providers, and even other financial lenders who are all part of a larger community,” he said.

The central bank advised negosyantes to ensure that they are borrowing or transacting with licensed financial service providers.

“It is also important for MSMEs to fully understand the terms and conditions of their loan contracts, their responsibilities as borrowers, and the consequences of defaulting on a loan contract. MSMEs are encouraged to ensure that they have the capacity to pay their obligations within the terms of their loan contracts,” the BSP said.

The DTI-ROG added that small businesses can also coordinate with their local Negosyo Centers or the Negosyo Center Online Portal to keep track on trainings, marketing opportunities, and other business development services available within their location.

“The DTI invests in developing MSMEs by allocating funding for programs such as the ‘One Town, One Product’ to provide product development assistance, or ‘Kapatid Mentor Me’ to provide mentorship modules. Participation of MSMEs to these programs are fully subsidized by DTI,” it said.

“We also advise small businesses to leverage digitalization to enhance their business operations (e.g., digitized bookkeeping, automated Point of Sale, etc.) or expand their consumer base (e.g., online marketing, last mile delivery services, etc.),” it added.