Low unemployment and more trade with more countries

There were two good pieces of data released by the Philippine Statistics Authority (PSA) recently. One was the low inflation rate of 1.9% for September, the other was the low unemployment rate of only 4% for August 2024 vs. 4.4% in August 2023.

In a press statement, Finance Secretary Ralph G. Recto celebrated these numbers, saying that “I am very glad of the back-to-back good news…. we expect more economic opportunities to be created, especially in the wholesale and retail trade sectors, as the holiday season nears and shopping peaks… The latest monetary policy easing due to the deceleration of inflation will also encourage further growth in consumption and investment that translate to more quality employment for Filipinos.”

In a separate press statement, Budget Secretary Amenah F. Pangandaman highlighted the low inflation rate, saying that, “This proves that we remain on track with our Agenda for Prosperity. Together with the rest of the Economic Team, we will continue implementing measures to reduce further inflationary pressures such as enhancing agricultural productivity, expanding logistics infrastructure, ensuring the efficient delivery of social services, and providing inflation-related subsidies.”

The labor force participation rate (LFPR) in August rose to 64.8% vs. 63.5% in the previous month. The LFPR is an indicator of optimism or pessimism of working age people about the local jobs market. If they think they can get a good and satisfying job, they go out and seek it and the LFPR goes up, usually 64% and higher. If people think the job market is bad, they pursue studies or just stay home and wait for better job opportunities and the LFPR goes down, usually 63% or lower.

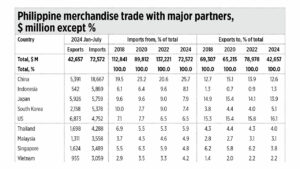

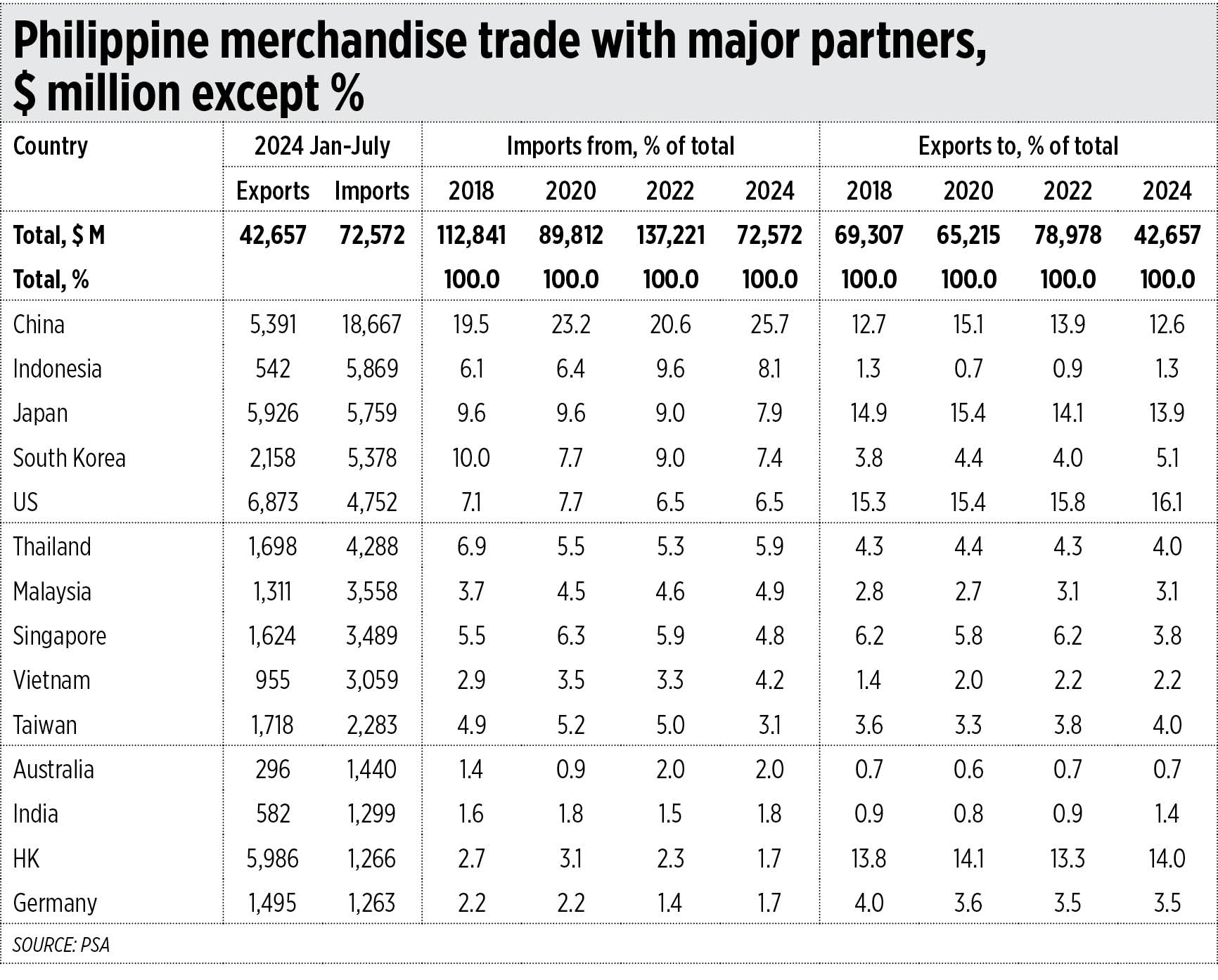

The PSA also recently released the country’s international merchandise trade statistics (IMTS) for July. I am particularly interested to know the value of our exports and imports in goods (services not included) with our major trade partners, so I checked the IMTS of previous years. The following trends can be seen.

The share of China in total Philippine imports keeps rising, from 20% in 2018 to 26% in January to July this year. The share of China in our exports remains flat at 13% from 2018 to 2024.

Indonesia has overtaken Japan, South Korea, and the US as the second biggest source of Philippine imports from 2022 to the present. But Indonesia is not buying much from the Philippines, with only a 1% share of total exports.

The share of Japan, South Korea, the US, and Thailand of total Philippine imports is declining while their share of total Philippine exports has flatlined.

Europeans are minor trade partners of the Philippines. The share of Germany, France, Italy, and Spain to total Philippine imports this year is only 4%, both among exports and imports (see the table).

{kind=link}

The above numbers seem to contradict the frequent narrative and surveys that say Filipinos distrust China. Of every $4 of Philippines imports, $1 is from China – from toys, shoes, and electronics to trucks, buses, and bulldozers.

So our piecemeal war-mongering defense and foreign affairs policy direction against China runs contrary to the trade appetite of average Filipinos who prefer to have more trade and commerce, more investments and economic partnerships with China.

We should focus on more trade and investments, more peace and diplomacy with more countries around the world, not more war mongering. We should spend more tax money on infrastructure, on more and bigger airports and seaports, on toll roads and train systems, on power supply and energy security. Then we can create more jobs and businesses for our people, and our LFPR and employment rates will remain high while our unemployment and underemployment rates will remain low.

Bienvenido S. Oplas, Jr. is the president of Bienvenido S. Oplas, Jr. Research Consultancy Services, and Minimal Government Thinkers. He is an international fellow of the Tholos Foundation.