My Economic Forecast for 2024 – 6.5%

In this column’s piece “Economic Forecast 2024” (Nov. 21, 2023), I presented a table showing the 2024 GDP growth forecast for the Philippines by the IMF’s World Economic Outlook (October 2023) which was 6.2%, the ADB’s Asian Development Outlook (September 2023) which was 6.2%, and Trading Economics (November 2023) which was 6.4%.

Recently, the ASEAN+3 Macroeconomic Research Office (AMRO) projected that the Philippines’ GDP growth this year would be 6.3%. See BusinessWorld’s story “PHL to grow fastest in the region this year — AMRO” (Jan. 19, 2024).

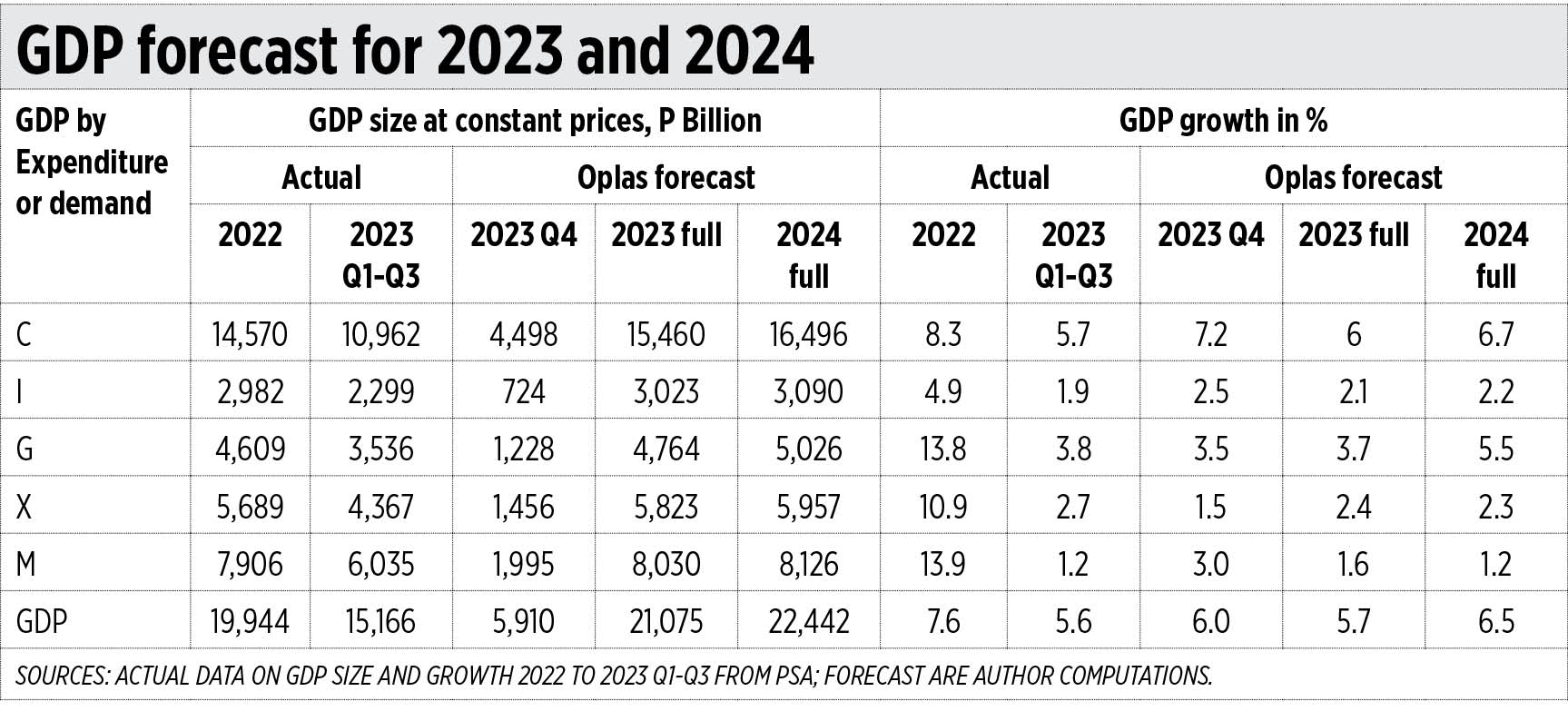

For the latest in my “Economic Forecast 2024” series (the second part came out on Nov. 24, 2023), I have produced my own forecast for the 4th quarter (Q4) of 2023 — hence full year 2023 — then my predictions for 2024. For the sake of brevity, I have taken the GDP by expenditure or demand and set aside GDP by industrial origin or supply side.

{kind=link}

GDP by demand is composed of Household Consumption expenditure (C), Capital formation or Investment (I), Government consumption expenditure (G), and net exports of goods and services (exports minus imports, X-M). In short: GDP = C + I + G + (X-M).

A forecast is only as good as the assumptions made. Mathematical and econometric models may be beautiful and sophisticated but if the assumptions are not realistic, then unrealistic numbers (positive or negative) will be generated.

I have made the following assumptions:

Household consumption (C), which is 73% of GDP, would grow in both 2023 Q4 and all of 2024 due to high consumer confidence. There are two reasons for this: when it comes to electricity demand, data from the Independent Electricity Market Operator of the Philippines (IEMOP) showed that average demand was 10,444 megawatts (MW) in Q4 2022 and 13,107 MW in Q4 2023, or a big 25.5% increase year on year (yoy).

In addition, vehicle sales data from the Chamber of Automotive Manufacturers of the Philippines, Inc. (CAMPI) and Truck Manufacturers Association (TMA) showed that total vehicle sales in 2023 reached 429,807 vs. 352,596 units sold in 2022, a big 21.9% increase yoy. See the report in BusinessWorld, “Vehicle sales surpass target in 2023” (Jan. 18, 2024).

Investment (I) is 23% of GDP. Foreign direct investment (FDI) and portfolio investment could tank but domestic investment would make up the gap. As reported in BusinessWorld, net FDI from Jan.-Oct. 2022 was $7.92 billion, and Jan.-Oct. 2023 it was $6.53 billion, a contraction of 17.5% yoy. Net foreign portfolio investment from Jan.-Nov. 2022 was $793.8 million, then contracted in Jan.-Nov. 2023 to $42.1 million.

But the decline in unemployment from 6.5% in November 2021 to 4.2% in November 2022, and 3.6% in November 2023 is a clear case that domestic investment is taking the weight when it comes to job creation.

Investments this year are projected to be high mainly due to the operation of the Maharlika Investment Fund and the attraction of more investments from other countries’ sovereign wealth funds and investment funds. I see about 5.5% growth over the 2023 level.

Government consumption (G) is 14% of GDP. It would keep a modest growth of around 2% yoy. Budget Secretary Amenah F. Pangandaman argued that “government needs to balance the gains from productive public spending especially infrastructure and safety net spending like Protective Services of Individuals and Families in Difficult Circumstances (PSIFDC) vs. the pains of heavy borrowings and high interest payment plus the need for higher taxation to retire those debt in the long-term.” That is a good and practical balancing act there, Madam Secretary. Thank you.

Exports of goods and services (X) would have minimal growth because of two things: merchandise or goods exports at $73.2 billion in Jan.-Nov. 2022 declined to only $67 billion in Jan.-Nov. 2023, a -8.4% change yoy. Meanwhile, OFW remittances from Jan.-Nov. 2022 of $29.4 billion increased slightly to $30.2 billion in Jan.-Nov. 2023, or growth of 2.8%.

Imports of goods and services (M) would have modest growth of around 3%. Merchandise or goods imports in Jan.-Nov. 2022 of $126.9 billion declined slightly in Jan.-Nov. 2023 to $116 billion. The net exports (X-M) is -10% of GDP.

The Top 5 export markets of the Philippines are the US, Japan, China, Hong Kong, and South Korea — they buy 61% of total Philippine merchandise exports. And all of them are experiencing economic hardships. Their growth performance in Q1-Q3 2022 and Q1-Q3 2023 respectively were: the US, 2.1% and 2.4%; Japan, 1% and 2.1%; China, 3% and 5.2%; Hong Kong, -3.5% and 2.8%; and, South Korea, 2.6% and 1.1%.

Such modest growth by our major trading partners is not conducive to the expansion of our exports. Luckily our neighbors in the ASEAN — like Indonesia, Malaysia, and Vietnam — are growing somewhat faster and they may purchase more of our excess exports.

The accompanying table shows the numerical results of these assumptions.

The Philippine Statistics Authority (PSA) will release the 2023 Q4 GDP data on Jan. 31. I will write about it and compare how the numbers in this exercise would fit or diverge from the actual performance of the Philippines economy.

Nonetheless, we should remain optimistic about the state of the country’s economy and business. The economic team remains intact despite the change in leadership at the Finance department. The new Finance Secretary, Ralph Recto, has the economics training, business partners, and a political network to advance market-oriented reforms.

Bienvenido S. Oplas, Jr. is the president of Bienvenido S. Oplas, Jr. Research Consultancy Services, and Minimal Government Thinkers. He is an international fellow of the Tholos Foundation.