Revenue challenges faced by new Finance chief

HONG KONG — As my family’s belated vacation here is ending, I see that Hong Kong as a tourist and investment hub is back to where it was in 2019, or even better. The big crowds at Central, Tsim Shia Tsui, Mong Kok and other areas in Kowloon, the huge volume of passengers inside long trains, the huge construction projects at the airport, these are among the reasons why I say this.

Hong Kong’s extensive infrastructure — its smooth wide roads, its huge suspension bridges, tunnels, and flyovers, its subway train-walkway-shop complexes, its large modern airport, its huge, long seaports, its brightly lit roads and streets, etc. — they were all built with little public borrowing. Until 2019, its public debt to GDP ratio was only 0.3%. This went up to 4.2% in 2022 and is projected to reach 7% this year. In contrast, the Philippines had a debt/GDP ratio of 37% in 2019, and this increased to 57.7% between 2022 to 2024.

If the Philippines, or at least the Metro Manila-Cavite-Bulacan area, would strive to be at par with Hong Kong at the current pace of infrastructure development in the country, I think it would take us at least 40 years get to where Hong Kong’s infrastructure is now.

But if we get huge infrastructure financing (both public and private), and the various political hurdles and bureaucracies (both national and local) are removed, perhaps we will do it in 25-30 years. And this is the big challenge facing the new Secretary of the Department of Finance, Ralph G. Recto.

The previous Finance Secretary, Benjamin Diokno, as leader of the economic team, laid down a good foundation. The Philippines’ GDP growth was high at 7.6% in 2022, and 5.6% in Q1-Q3 2023 — the third highest among the world’s top 40 largest economies last year. Revenues overall have recovered even without any major tax hikes. Hats off to Sir Ben.

Here is the situation and the challenges the new secretary will face at the Department of Finance (DoF) in 10 points:

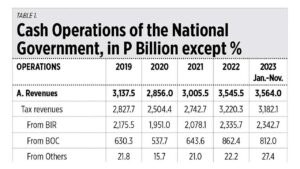

1. Expanding the tax base. Considering revenues were at P3.45 trillion in 2022 and are projected to be around P3.90 trillion in 2023, the target of at least P4.5 trillion this year should be attainable even without tax hikes because the recently enacted law Ease Of Paying Taxes (EOPT) Act (RA 11976, signed Jan. 5) should be able to expand the tax base. Other proposed revenue bills can help if they are enacted soon.

2. A busy BIR. The Bureau of Internal Revenue (BIR) in particular can target at least P3.3 trillion (about 67% of total revenues) this year as the EOPT law applies more to it than to the Bureau of Customs (BoC) and broadening of the tax base applies more to domestic than international business.

3. The need to control smuggling. The BoC may target collecting P1.8 trillion by significantly controlling smuggling and illicit trade. From the estimates Representative Joey Salceda gave last October, tobacco smuggling alone results in about P60 billion/year in revenue losses. The BoC plus other lead enforcement agencies like the Philippine National Police and the Coast Guard should work harder in controlling illicit trade because their annual budgets are huge and come from taxes, so they should strive to control tax leakage.

4. Keeping the budget deficit under control. In partnership with the Department of Budget and Management, the Finance department must control some spending so the budget deficit this year does not exceed P1.4 trillion and the deficit/GDP ratio is limited to 6.5% or lower.

5. Keeping a lid on borrowing. Financing or borrowings, which averaged P2.2 trillion/year from 2020-2022, should be controlled so as not to exceed P1.8 trillion this year. If revenues increase significantly and the deficit is controlled, the need for borrowing is reduced and interest payments will be reduced in the succeeding years.

Accompanying this column is a table featuring the actual numbers in cash operations from 2019 (pre-lockdown) to 2023 (post lockdown) and on which my proposals for fiscal targets in 2024 are based (see Table 1).

{kind=link}

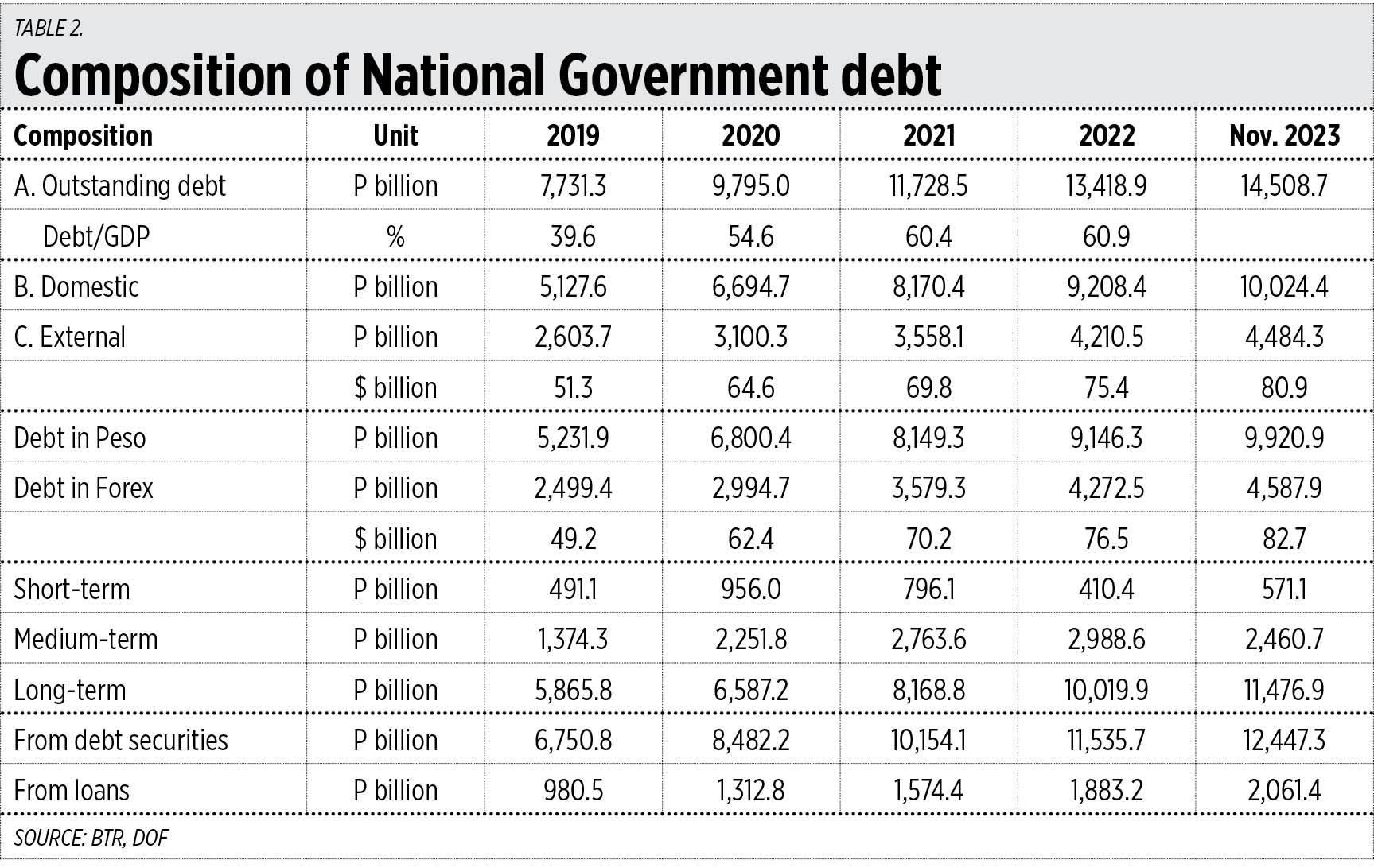

6. Lowering the debt/GDP ratio. The outstanding debt stock (excluding contingent liabilities) should peak this year at around P16.5 trillion, then plateau for a year or two, and begin to decline by 2027. We should strive to bring back 2019’s debt/GDP ratio of 40% by 2028, down from 61% in 2022.

7. Avoiding long-term loans. We should reduce long-term loans even if the interest rates are lower because they create a big moral hazards problem. Agencies contracting the long-term debt can afford to be wasteful because the ones that will pay these off will be two to four administrations (six to 20 years) away. In November 2023, long-term debt constituted 79% of the total outstanding debt, up from 76% in 2019. Leave long-term financing to PPP projects and Maharlika funding. The vetting process and financial discipline in private financing is more strict and less political than government and foreign aid/ODA funding.

8. Avoiding forex risks. There is also a need to reduce borrowings from commercial or debt securities, not only because of higher interest rates, but also due to rising forex risks as the US$ is under constant and rising threat of large-scale instability because of huge increases in US federal debt.

Accompanying this column is a table of the actual numbers in public debt and their distribution (see Table 2).

{kind=link}

9. Controlling spending. The major spending control challenges must be addressed by the economic team as a whole. These include reforming the huge and ever-rising military and uniformed personnel (MUP) pension which may reach P200+ billion this year alone. Then there are the subsidies which seem to stretch forever, with no timetable — freebies should have a limit. And war-mongering lobbies that say that we should buy very costly jet fighters, battleships, submarines, and missiles should be kept at bay. Our priority should be more domestic infrastructure and more job creation here, not more war mongering on faraway shores.

10. Sustaining the high GDP growth target. We ought to keep a high GDP growth target of 6.5% to 8% yearly until 2028 and beyond. Our deficit/GDP ratio and public debt/GDP ratio can easily decline if the denominator, our GDP size, expands fast at sustained level.

Ralph Recto has the maturity and wisdom of a seasoned legislator and statesman (he has been a senator, a congressman, and secretary of the National Economic and Development Authority or NEDA). His overview of economics and politics has been sharpened by long years of government experience and he has an extensive network with the public, especially tax-paying entrepreneurs and investors.

I extend my congratulations to Mr. Recto for taking up the challenge. The best is yet to come, here’s to a wealthy and prosperous Philippines.

Bienvenido S. Oplas, Jr. is the president of Bienvenido S. Oplas, Jr. Research Consultancy Services, and Minimal Government Thinkers. He is an international fellow of the Tholos Foundation.