Stabilizing growth with low inflation, low unemployment rates, and more PPP investments

(Part 4)

There were three positive economic developments last week.

First, the Philippine Statistics Authority (PSA) reported that November’s inflation rate was a low 4.1%. This was down from 4.9% in October and 8% in November 2022, or just half of the level a year ago.

Second, the PSA also reported that the unemployment rate in October was a low 4.5%. This is very significant because it is the lowest unemployment rate the country has seen since April 2005. See these reports in BusinessWorld: “Inflation cools to 4.1% in November” (Dec. 6), and, “Unemployment rate drops to 18-year low in October” (Dec. 8).

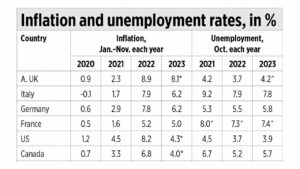

I have consolidated and summarized the monthly inflation data plus comparable months’ unemployment data of other countries in an accompanying table. Group A is composed of the G7 industrial countries, Group B is made up of the big South Asian economies, and Group C contains the big East Asian economies. The Philippines has the highest inflation rate this year among its neighbors in East Asia and is comparable to those in Italy and Germany (see the table).

{kind=link}

Budget Secretary Amenah Pangandaman has correctly observed that “Fiscal consolidation is bearing fruit, the high GDP growth of 5.6% average for Q1-Q3 of 2023 is creating more jobs, the January-October average unemployment rate of 4.6% is lower than the 5.3% to 6.4% target for 2023 in the Philippine Development Plan. Our public spending especially in hard and soft infrastructure is helping expand labor productivity of our people and business dynamism.”

The third piece of good news last week was the signing into law by President Ferdinand Marcos, Jr. of the Public-Private Partnership (PPP) Code of the Philippines (RA 11966) on Dec. 5.

The new PPP Code will do many things: 1.) it will establish a stable, predictable business and financing environment for public and private collaboration; 2.) it will consolidate all legal frameworks and clarify ambiguities in the existing Build-Operate-Transfer (BOT) Law which was last amended in 1994; 3.) it will streamline project implementation process and update approval thresholds for national PPP projects; 4.) it will improve the framework for unsolicited proposals and it establishes a predictable tariff regime to protect public interest; 5.) it will promote autonomy in implementing local PPP projects; and, 6.) it will institutionalize the PPP Governing Board, Project Development and Monitoring Facility, and the new Risk Management Fund, among others.

The Marcos Jr. administration has identified 197 infrastructure flagship projects (IFPs) with combined investments of P8.7 trillion; 41 of these 197 IFPs will be financed through PPPs.

National Economic and Development Authority (NEDA) Secretary Arsenio Balisacan, as head of the PPP Governing Board, will issue the Implementing Rules and Regulations (IRR) within 90 calendar days from the law’s effectivity.

PPP Center Executive Director Cynthia Hernandez had an optimistic view and said that: “The PPP Code of the Philippines is a landmark [piece of] legislation that will prioritize job creation through the promotion of trade and investments, improve infrastructure, encourage more financially viable, well-structured and high-quality PPP projects to be delivered to Filipinos. The PPP Center looks forward to shepherding the stakeholder consultation process that shall be conducted to prepare the IRR of the new law. We want to make ensure a smooth transition period and to continue the progress that has already been achieved.”

Congratulations to the economic team plus the PPP Center leadership.

Back to Philippines inflation.

The top three sources of inflation from January to November were Food and non-alcoholic beverages (8.1%), Alcoholic beverages and tobacco (10.9%), and Restaurants and Accommodation Services (7.6%). Double-digit inflation continues for rice, fruits, and vegetables.

Among the reasons for this that I see is the slow but steady incursion and conversion of agricultural land into solar farms, on top of their conversion into residential and commercial land use. The average rice yield in the Philippines is about 3.5 tons/hectare, and with two harvests per year (three harvests for well-irrigated lands but this is not big) means seven tons/hectare/year.

Solar farms require about 1.5 hectare per 1 MW solar capacity. So, a 500-MW solar farm will require about 750 hectares of land, including roads, fences, etc. If that 500-MW solar farm was previously a rice field, then it has permanently displaced or deprived the country of 5,250 tons/year of rice (7 tons/hectare/year x 750 hectares). That is not good.

There are thousands of MW of solar capacity coming on stream in the next few years. Most are inland and some are floating solar in lakes and dams. Big solar farms on lakes will keep sunlight from penetrating the lake water and thus affect the food chain, and this can lead to reduced harvest of inland fishery.

While I am hopeful that more PPP investments, more productivity-enhancing infrastructure projects, more fiscal consolidation, more trade and economic liberalization will help stabilize food and consumer prices in the long term, I am less optimistic that this can be achieved when more agriculture and forestry land are converted to expand solar and wind farms to “save the planet.”

As a developing country with a big population, we should prioritize more food production, more price stabilization, more growth and job creation over hazy climate and ecology goals. We are lucky that El Niño 2023, that started last April, has not led to the feared “more drought, more warming.”

The previous articles in the “Stabilizing growth” series are, Part 1, “Stabilizing growth: Declining inflation and unemployment rates” (Nov. 9); Part 2, “Stabilizing growth of the fastest growing major economy in the world” (Nov. 14); and, Part 3, “Stabilizing growth via peace and order and free trade” (Dec. 5).

Bienvenido S. Oplas, Jr. is the president of Bienvenido S. Oplas, Jr. Research Consultancy Services, and Minimal Government Thinkers.